Axis Tactics 15th April, 2026 - Global Trends Update

| Strategy Primer for Conservative Investors | Global Tactical Trends across Indices, FX, Soft Commodities & Metals | Positions Update in Gold, Silver and Crypto |

If you already maintain an active portfolio, advisory relationship or trading account with one of our Group Companies, please reach out to your usual contact or otherwise via email on info@axis-im.com, for a full access code to all sections in this Newsletter, inclusive of (i) Pay-Walled content on Specific trade recommendations, (ii) Entry and Exit timings and (iii) Risk Management Parameters.

Access Codes also available for Trusted Media contacts.

For more information on what we do and the services we offer, please visit www.axis-im.com.

Strategy Primer for Conservative Investors

“Time in the Market” beats “Timing the Market”

Often true but not an absolute truth, depending on your choice of statistics, data sets and when you start. Nevertheless, for Investors that have a modest or conservative attitude to risk, tactical trading and frequent sweeping changes to asset allocations are just not viable often due a lack of time and energy available to devote to such matters - hence the popularity of the “buy, hold, forget” approach.

Additionally, most investors do not use leveraged instruments and do not hedge their downside risks.

We start by setting out some considerations on how traditional long-only conservative investors can use the guidance we provide, whilst remaining well within their low-touch, low stress and low effort conservative risk lane.

Just one statistic to present this point - the CBOE Dispersion Index for the S&P 500 Index is currently on the high end of its longer term range, at 37.44, which means the difference in expected returns between the worst performers and the best ones, is likely to be far far wider than in typical circumstances*.

Put another way, simple index tracking doesn’t work as well when the Dispersion Index is this elevated and to illustrate:- the S&P 500 Index itself has not moved constructively over the last few months as the US IT Sector fell sharply while both Energy and Materials Sectors rose over 20%. Good performers are cancelled out by the weaker ones.

Hence, should conservative risk investors seek to take some steps at all, these are our suggestions:-

When presented with market intelligence indicating that the relevant markets (we cover analysis on Indices, Regions & Industry Sectors) are over-extended or otherwise at risk of a correction, consider :-

Raising a little cash for later deployment, by taking profits and reducing the largest positions. Holding in high income instruments for the short term keeps the funds at work in the interim. Overall performance would have been materially enhanced by selling/reducing on the sell signal and re-investing shortly after.

If reducing market exposure is not desired, rotate/reduce from Sectors that are expected to Lag or have become frothy and over-extended, increasing the weighting into Sectors that are expected to Lead (and are hence in a recovery phase). Again, overall performance would have been materially enhanced by rotating or reducing US Tech exposure and allocating a greater weighting to Energy or Materials. Usage of simple ETFs to make modest adjustments, that’s it.

This still corresponds to Zero “Time out of the Market” (or almost zero if booking profits from time to time) but with a vastly improved investment return profile.

Thematic Longer Term Investing has a different methodology, as the time horizons are measured in years, where the trends are global in their impact and much longer term. Less need for intervention and adjustments during the investment lifecycle but very high conviction in the themes is required at the outset as well as Investor confidence in taking the long term outlook.

For our Family Office Portfolios and Managed Accounts, we operate both styles.

* The mathematics is based on normal distribution, so the higher the Dispersion Index, the higher the idiosyncratic risk. This leads to a greater number of performance surprises at both Individual Stock level and Sector Level, to the upside and downside. As the SKEW Index is also elevated, fatter tails in the distribution indicate an increased likelihood of an extreme market event - as expected since there are a few wars going on…both together indicate a nimble approach will outperform a passive approach…

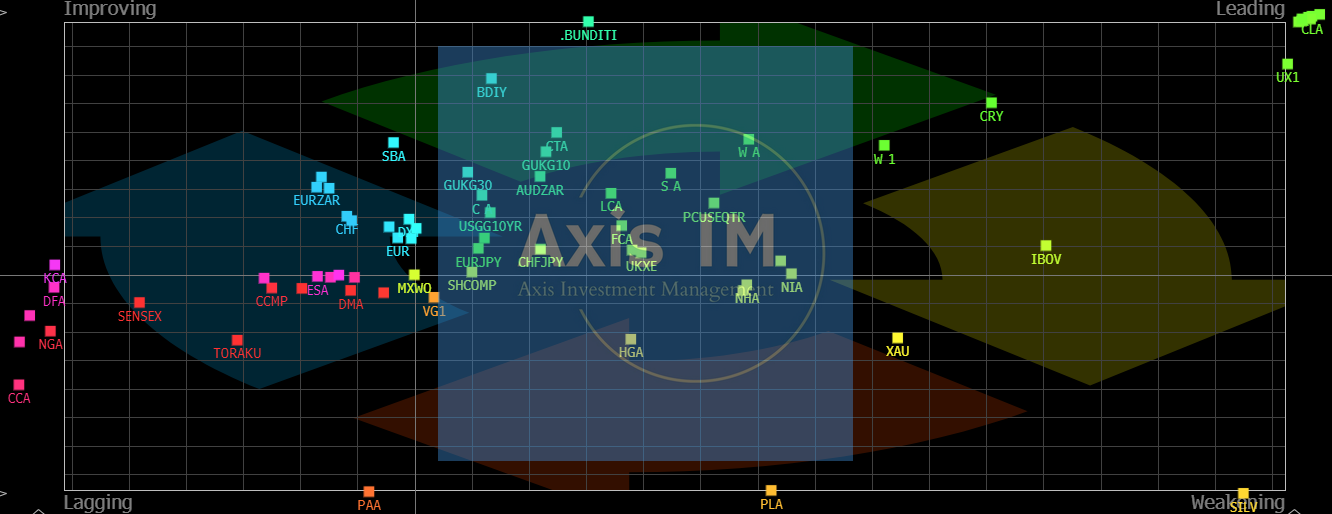

Global Macro Trends - Indices, FX, Commodities

For precise entry and exit points, as well as preferred issuers and equity names, please contact us. The below is indicative and macro-based guidance.

(Axis IM Analytics using Bloomberg RRG & Axis IM Proprietary Data)

Soft Commodities - We have recently observed some stabilisation in Robusta Coffee, Arabica and also Cocoa, after multi-week falls in prices. Active Investors would know that we had held a conviction short position on Coffee for several months (both Robusta and Arabica) and have recently closed those positions. Same applies for Cocoa. For all three, we are watching for a potential recovery in price trend. Soybeans, Cotton and Wheat seem to be well placed. Cotton has moved from 61 to 74 since February.

Metals - All four Precious Metals are presenting lacklustre trend indications. There is a lag with this type of analysis, nevertheless we would consider this as a sign for caution in Gold, Silver, Platinum and Palladium. We have active trades in these, please see section below.

FX/Crypto - Major FX appears rangebound, as USD Index, USD/CHF and EUR/USD are all hugging the cross-hairs, not compelling directionally. Bitcoin and Ether are on the borderline of improving but no confirmation of trend as yet. We would typically cross-check against our other tools to reinforce or de-bunk any trade ideas before proceeding. We have active trades in these, please see section below.

Indices - Brazil Bovespa (one of our favourites since last year) has continued to rocket. We have owned Petrobras (both regular and preferred) as one of our most favoured holdings. Whilst the IBOV is still in the leader zone, we are vigilant for a break in trend or a decline in momentum, at which point we expect to check out and re-allocate elsewhere. US Tech and EU Indices seem to have commitment issues, too close to the cross-hairs to rely on this study in isolation. US (S&P) & India are still in the Lag zone (only just) so separate confirmation of stability may soon elucidate buying opportunities. China’s recent upward momentum seems to be in decline but separate analytical confirmation is required.

Other observations : All the Oils (Crude, Brent, Heating Oil) as well as EU and US Volatility are still far up and to the right within the Leader Zone. Given the lag in this data and the speed at which events are shaping up, we would certainly cross-check with shorter term tactical tools before entering any positions on these. Gilt Yields in both the UK and US are both Leading. Continued strength and leadership in these might tip the balance to the downside in both UK and US Equities.

We are constantly corroborating these trends with our other analytics tools. As stated above, those who have access to our trading positions comments will already know our views on these, entry and exit points as well as other tactical trades we recommend.

Positions Update - Gold, Silver, Crypto

For current & precise entry/exit levels and intra-day position updates in real-time, please reach out to your Axis IM directly.

If you would like to view the Investment Recommendations Section below, please request access from your Axis point of contact.

Keep reading with a 7-day free trial

Subscribe to The Axis Tactics Newsletter to keep reading this post and get 7 days of free access to the full post archives.